Solution visibility can be tough when we’re pummeled with daily reminders of downside risk. However, it’s entirely possible to sketch a blueprint of our bridge back to normalcy, or some semblance of it. That task is much more doable in May than it was in just April or March. The interconnecting trusswork to this design is unparalleled global scientific collaboration, and the tools being used to construct it include near-endless pools of compute power, cheap genome sequencing costs, widened communication pipelines among research institutions, and access to stockpiles of intellectual property previously held captive in the vaults of big pharma. As an NYT article succinctly stated, “While political leaders have locked their borders, scientists have been shattering theirs, creating a global collaboration unlike any in history. Never before, researchers say, have so many experts in so many countries focused simultaneously on a single topic and with such urgency. Nearly all other research has ground to a halt.”

As investors, we’re intimately aware of the impact of volatility surging to an 85 print on the CBOE Market Volatility Index; the S&P 500 plunging 34% across 23 consecutive trading sessions, nonfarm payrolls plummeting to 20.5 million with unemployment spiking to 14.7%. All while the global population scrambles in our personal lives to mitigate the invisible threat.

However, beneath the violent surface waters, globally coordinated efforts ensue across academic, government, business, and scientific institutions, narrowing down the universe of compounds in efforts to fast-track candidate therapeutics and vaccinations. Details behind this specific process entail narrowing 8,000 known drug compounds to 77 based on millions of permutations, a project that supercomputing tackled in two days rather than the months it would have taken traditional computers. Additionally, patient trials ramp at a global scale in days rather than their usual weeks/months cadence. All of this unprecedented speed largely has been enabled by unparalleled molecular insights afforded by modern technology.

Borrowing Keys to a $400M+ Machine

NVIDIA Corporation [NVDA] provided specific context to this last week on its earnings call. Its CFO, Colette Kress, cited how 27,000 NVIDIA graphical processing units (“GPUs”) enable the silicon horsepower behind the Oak Ridge supercomputer being used by Coronavirus researchers. If you consider the average selling price of roughly $8,000 for the V100 GPU designed into these compute clusters, this translates into a $216 million outlay solely for this component. Adding on storage, networking, and ancillary hardware would likely double the total system cost. Any other researcher in any other prior period would have to request to borrow the keys to a $432 million machine, or attempt to raise grant funding to build it, just to test a drug candidate. We truly have unprecedented tools at our disposal.

Piecing all of this together, while simultaneously tuning out the armchair virologists in our ears, is always easier in theory than in practice. However, the necessary exercise to thinking through our current environment as investors is akin to the one Apple, Inc has built into its engineering ethos: we must look at the problem with a beginner’s mind. Markets respond to changing probabilities, not definitive declarations of certainty. We see the aggregate of these global scientific efforts as a large driver of the market’s recovery since its March 23rd bottom and reason for continued progress along its path out of it going forward.

The Playbook is Broken

Traditional recession playbooks telegraph a flight to safety: sell divergence (e.g. the “FANGs”) and buy convergence (e.g. IBM and GE). The deep-value crowd typically joins in chorus, gearing up to be vindicated by their long-awaited mean reversion. However, this playbook is broken. Massive demand shifts underway in today’s disruption are enabled by the exact digital platforms that technology companies have been assisting to deploy over the past decade+. This in turn has led to disproportionate success, stock price performance wise, in issuers that comprise larger portions of “growth” indices, in comparison to “value” or “blend.” The good news here is these trends will likely extend far beyond being one-and-dones. We believe odds are more attractive for sustainability than simply a demand pull-forward.

Evidence of the bifurcation can be seen in YTD results across the style indices (as of May 26th close):

- Russell 1000 Growth: +3.27%

- S&P 500: -6.64%

- Russell 1000 Value: -17.06%

Using Electronic Payments as a Lens

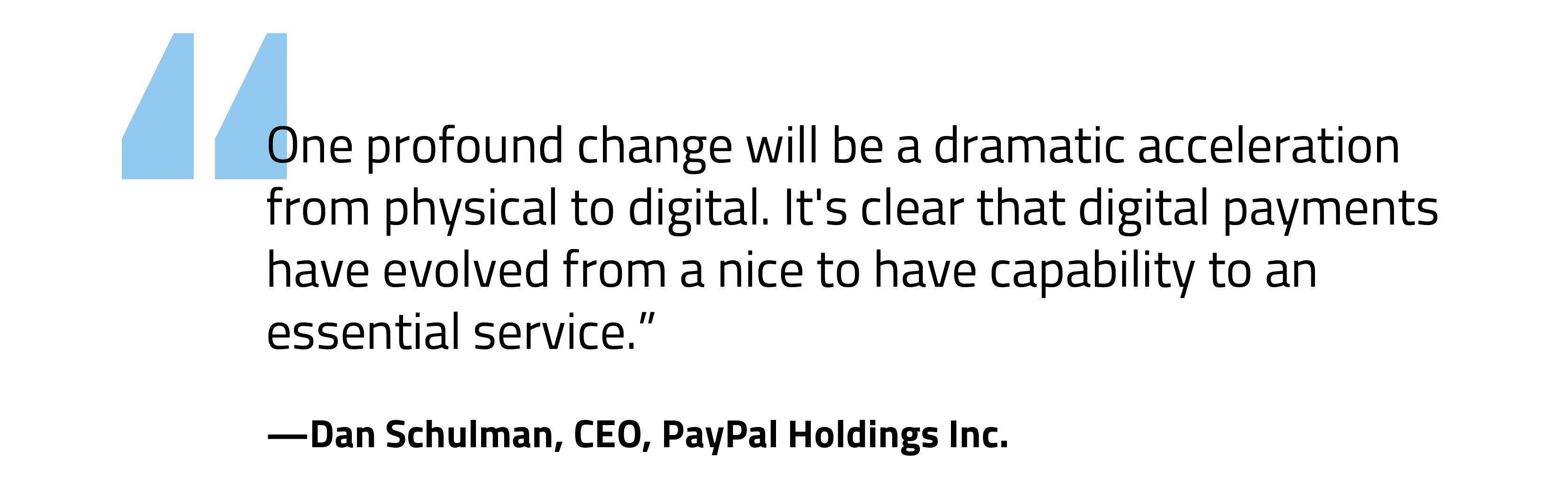

Sifting through April/May evidence at the underlying-position level, the answer of why this is happening becomes clearer. Consider, for example, the competitive landscape within the payments sub-sector of financial services today. Paypal made note of how digital payments have shifted from “nice to have” to “essential” in just a few months. Aside from increased consumer disinterest to pass physical paper bills at point-of-sale terminals—this category alone comprised $18 trillion of retail spend across 2019—customers are shifting to online shopping levels that rival Black Friday and Cyber Monday in May. The company also experienced a surge net new customers, with April bringing in 7.4 million total, representing 27% annualized growth off its March base.

Square also chimed in with similar signs of digital use acceleration. In the course of four weeks Cash App customers with direct deposit grew from 3 million to 14 million. Another narrative has been unfolding regarding these platforms’ inherent scalability when it comes to economic stimulus payments. While banks have had to prioritize larger PPP loan originations, simultaneously increasing ire among its small business customers, the electronic payment platforms have stepped in to fill an important gap. Square and Paypal collectively originated $1.5 billion in PPP loans with $12k–35k in average loan origination size. Aside from the speed and ease of PPP direct deposit, customer loyalty undoubtedly has accrued to the benefit of the electronic payment vendors at the detriment of traditional banks.

With a global footprint of customers, the payments vendors also afford us visibility into geographies that started to ease their respective sheltering efforts earlier than the US, such as Germany and Austria. Paypal has noted how online behaviors in these geos remain elevated at 2–3x pre-COVID levels even after a few weeks of reopening.Sub-sector

Exposure Differences Are Meaningful

All of this also underscores our view of why growth equity exposure is essential for long-term investors. Growth stocks have evolved from hype-based issuers with arbitrary valuations to real cash-flow generating businesses with far better sustainability. Index composition differences between the Russell 1000 Growth Index and the S&P 500 Index highlight reasons for this. Payments comprise over 70% of the Russell 1000 Growth Index’s financial services exposure, whereas traditional banks make up just 0.5% of the sector. For the S&P 500, banks comprise 13% whereas payments are 30%. We don’t see the consumer shift towards digital payments, away from physical, abating anytime soon. Therefore, disparity in outcomes is likely to continue as results fold into each respective index, especially as the banks attempt to squeeze net interest margin with near-zero overnight rates.

Commentary from Boots on the Ground

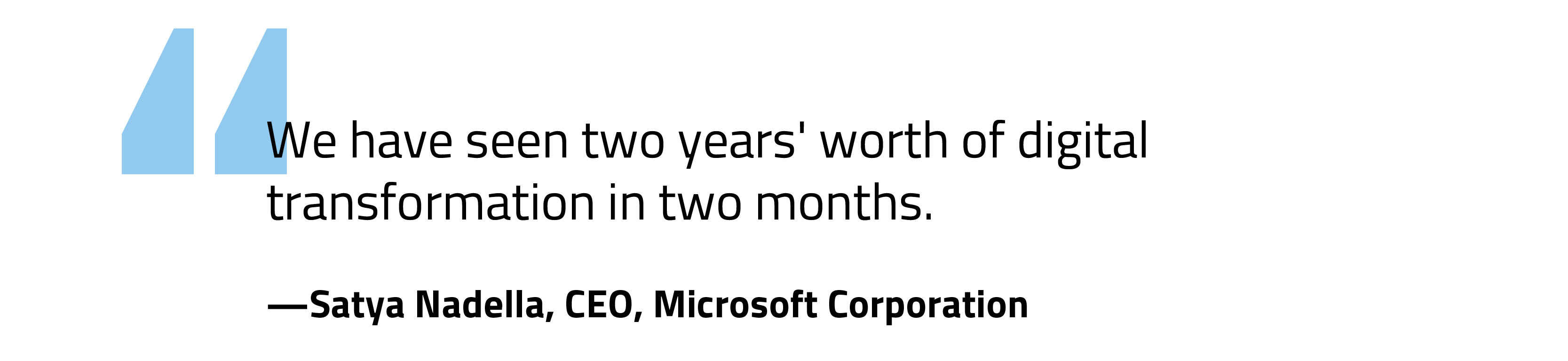

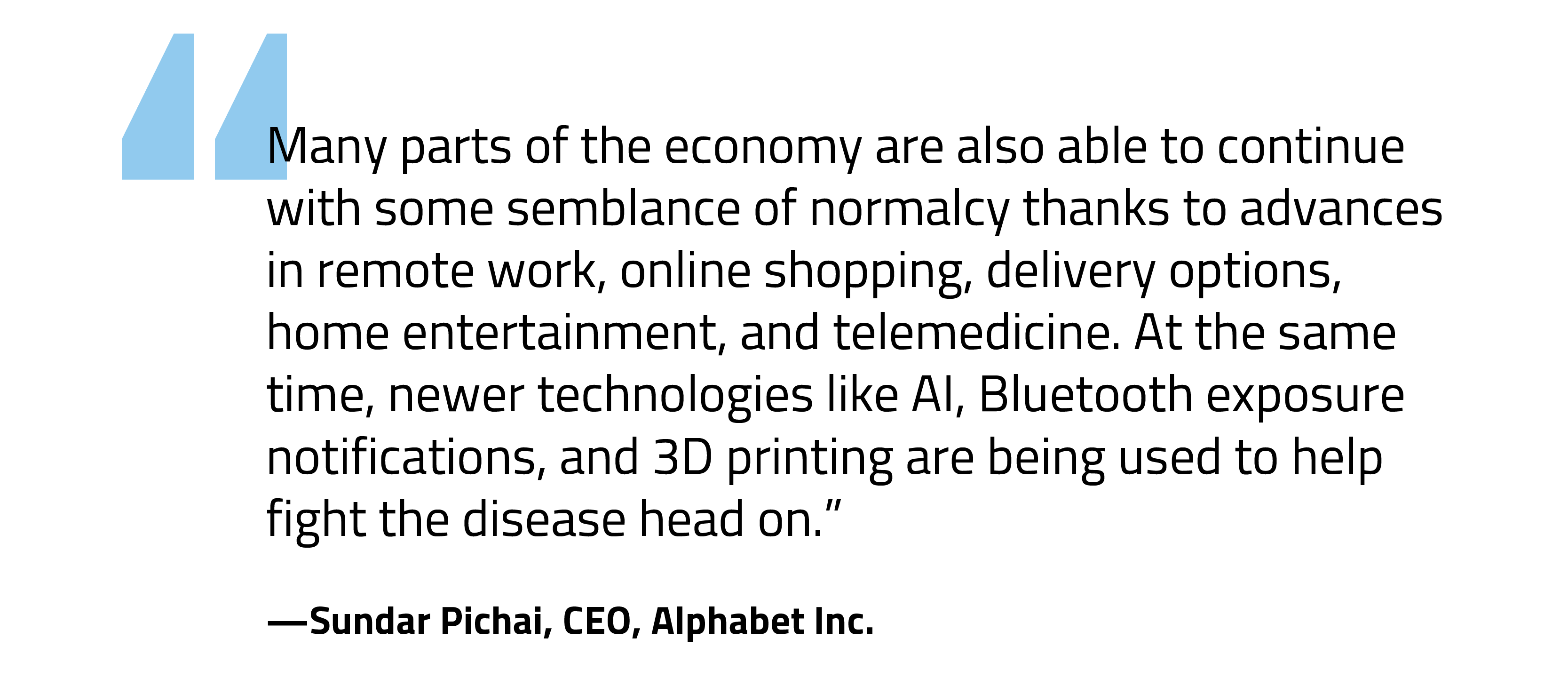

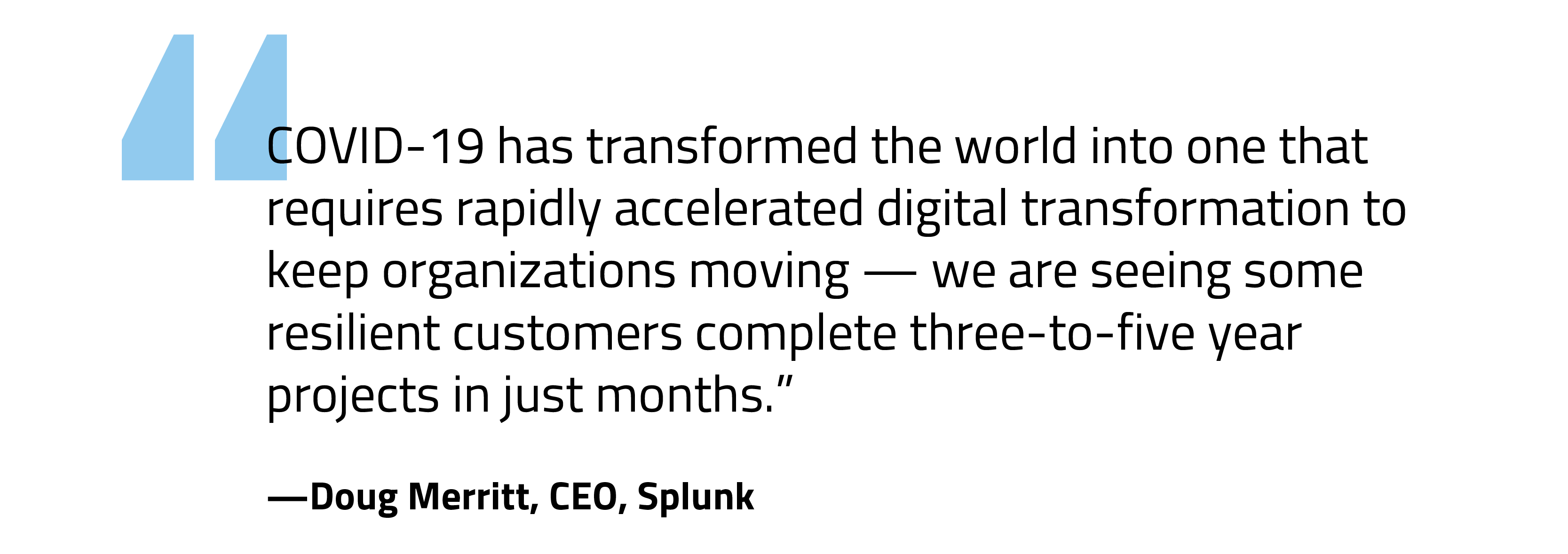

Although we chose to highlight trends unfolding in payments, similar themes can be found across all sources of economic output. Some commentary from 1Q earnings that echo this sentiment:

Pivoting a global population of 7.6 billion humans and the $86 trillion of GDP they were creating is no easy feat. This entire situation is highly dynamic, and many obstacles remain before we’re anywhere near our 2019 run-rate of economic output. From an investment strategy perspective, this environment has provided the ultimate stress test, one that reveals the true stripes of an investment strategy. When the exogenous risk ultimately arrives, it tends to separate strategies heavily reliant upon back-tested ideas sounding good in practice from those with stronger adaptability and staying power. Today that exogenous risk has arrived in the form of a global pandemic. As we assess how Growth Equity’s actual results stack up against expected, the good news is that the exact same factors we’ve structured our portfolio to disproportionately benefit from over the next decade are unfolding at an accelerated clip.

To access our latest SWS Growth Equity strategy fact sheet, click here.